VSME

Advisory

Climate Footprint

EU-project

The VSME standard explained: An in-depth overview of the Basic Module and the Extended Module

Feb 18, 2026

ESG reporting (VSME) has become an integral part of many companies’ reality. Small and medium-sized enterprises increasingly face demands for ESG data from customers, banks, and business partners. VSME has been developed as a practical and concrete response to these requirements, providing companies with a common framework for structured sustainability reporting.

VSME is based on the widely recognized EU sustainability reporting framework, the Corporate Sustainability Reporting Directive (CSRD). It is designed to consolidate ESG efforts in one place, create clarity, and ensure that sustainability initiatives support the company’s overall strategy. VSME consists of two modules that together provide a structured and flexible foundation for sustainability reporting.

The Two Modules in VSME Reporting

The Basic Module

The Basic Module forms the foundation and includes the core ESG disclosure requirements most companies encounter from customers, banks, and business partners. It provides a consolidated overview of climate, environmental matters, workforce issues, and responsible business conduct.

The Comprehensive Module

The Comprehensive Module builds upon the Basic Module and goes deeper into strategy, targets, risks, and governance. It is relevant for companies that wish to work more systematically with sustainability or that face increasing stakeholder requirements. Together, the two modules enable companies to consolidate ESG efforts in one place and work in a structured manner as the ESG evolves into the fundamental business model.

The Basic Module in VSME: What Must Be Reported

The Basic Module is structured around clearly defined data points that together provide a basic representation of the company’s ESG profile. The objective is not to create complex reporting, but to ensure consistency, transparency, and comparability. At the same time, the Basic Module allows companies to begin their ESG journey from a solid starting point without allocating excessive resources to reporting burdens and internal communication.

Below is an overview of what each disclosure requirement (sub topic) entails in practice, based on guidance from the Danish Business Authority.

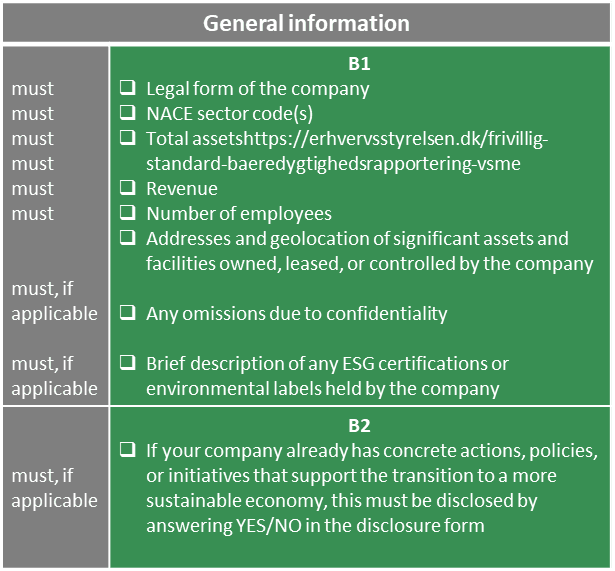

B1 - Basis of Preparation

This disclosure requirement establishes the framework for the entire report. It includes fundamental company information such as legal structure, industry classification, key financial figures, and number of employees. It also covers information about significant assets and their geographic location.

The purpose is to create context for the ESG data and ensure that stakeholders understand the company’s size, structure, and geographic footprint. Any omissions due to confidentiality must be clearly stated, and existing ESG certifications or environmental labels may be described where relevant.

B2 - Practices, Policies, and Future Initiatives for Transitioning to a More Sustainable Economy

This data point assesses whether the company has implemented concrete sustainability initiatives or established relevant policies. The response is provided as a yes or no.

If initiatives are in place, they can be briefly described. These may include energy efficiency measures, social initiatives, or responsible procurement practices. The focus is on direction and prioritization rather than detailed reporting.

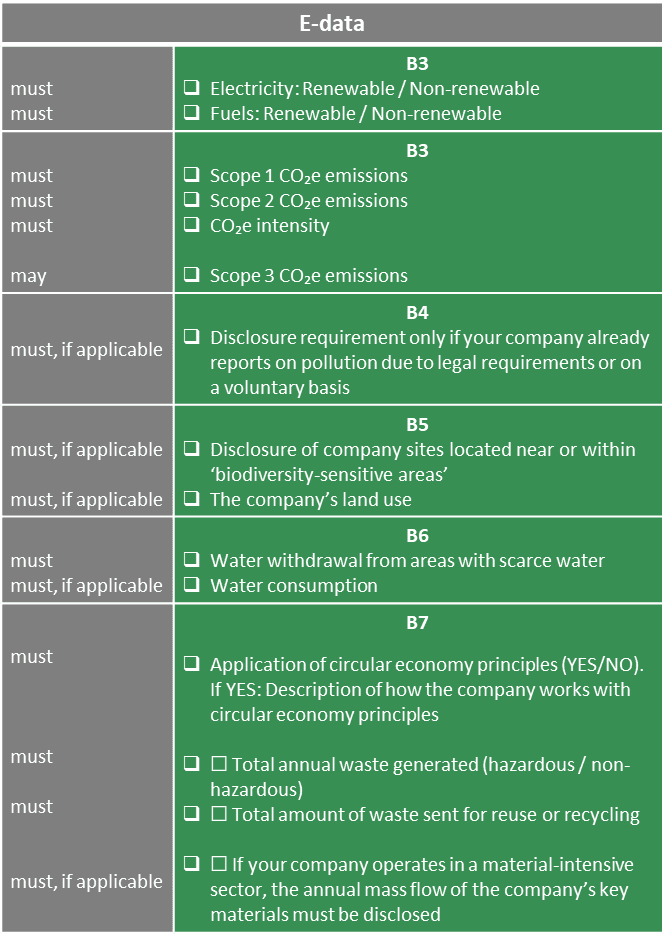

B3 - Energy and Greenhouse Gas Emissions

This is one of the most central disclosure requirements in the Basic Module. It includes reporting on energy consumption divided into electricity and fuels, as well as whether the energy originates from renewable or non-renewable sources.

Additionally, Scope 1 and Scope 2 CO₂ emissions are reported, along with CO₂e intensity. The purpose is to provide a clear picture of the company’s direct and indirect climate impact.

B4 - Pollution of Air, Water, and Soil

This requirement applies only to companies that already report on pollution of air, water, and soil due to legal obligations or voluntary schemes. It focuses on existing reporting rather than new measurements.

The objective is to ensure that significant pollution is not omitted where it is already known and documented.

B5 - Biodiversity

This section evaluates the company’s physical location in relation to biodiversity-sensitive areas. It assesses whether the company operates in or in close proximity to areas of high ecological value.

Where relevant, total land use may also be included. The focus is on potential impact rather than detailed environmental analysis.

B6 - Water

This disclosure requirement concerns the company’s use of water resources. Data points include water abstraction and total water consumption, where relevant.

The purpose is to identify whether the company has a significant water footprint, particularly in water-stressed regions or production-intensive processes.

B7 - Resource Use, Circular Economy, and Waste Management

This section covers the company’s handling of materials and waste. It includes a yes or no indication of whether the company applies circular economy principles, along with a short description if applicable.

Additionally, total waste volumes are disclosed, divided into hazardous and non-hazardous waste, as well as the share that is reused or recycled. Material-intensive companies should also report annual material flows.

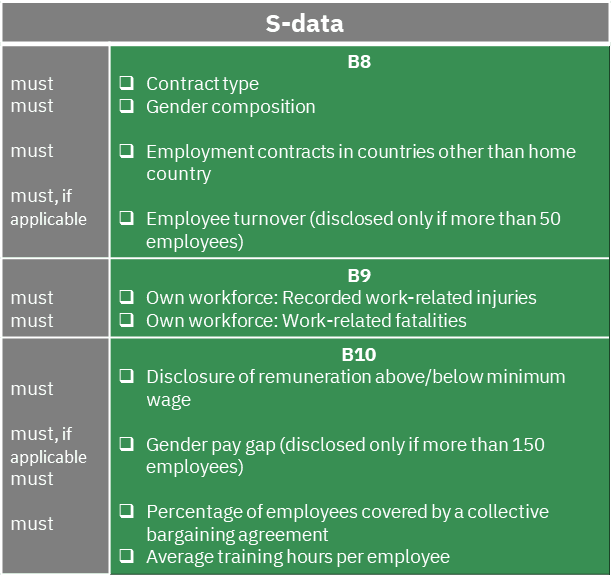

B8 - Own Workforce: General Characteristics

This disclosure requirement provides an overview of the workforce, including contract types, gender distribution, and any employment outside the national market.

For companies with more than 50 employees, employee turnover should also be included. The purpose is to provide insight into workforce composition and stability.

B9 - Own Workforce: Health and Safety

This section reports on occupational health and safety, including recorded workplace accidents and any work-related fatalities.

Although relatively narrow in scope, it is important as it provides a clear picture of workplace-related risks and health.

B10 - Own Workforce: Remuneration, Collective Agreements, and Training

This requirement focuses on compensation and skills development. It includes information on remuneration relative to collectively agreed minimum wages, the share of employees covered by collective agreements, and the average number of training hours per employee.

For larger companies, gender pay gaps should also be included. The purpose is to shed light on fair pay and investment in employee development.

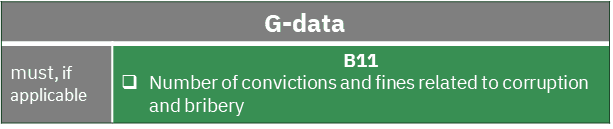

B11 - Convictions and Fines for Corruption and Bribery

The Basic Module concludes with a governance-related disclosure. It includes reporting on the number of convictions and fines related to corruption and bribery, where relevant.

This data point functions as a transparency mechanism and signals the company’s approach to responsible business conduct.

The Comprehensive Module in VSME

The Comprehensive Module is ideal for companies with ESG ambitions, as it connects sustainability directly to the business model, strategy, targets, and risks, making ESG an integrated part of core operations. It also provides a solid decision-making foundation and necessary documentation to build even more credibility with customers, investors, and other stakeholders.

Where the Basic Module creates overview and structure, the Comprehensive Module goes deeper into the interconnections between business, climate, people, and governance.

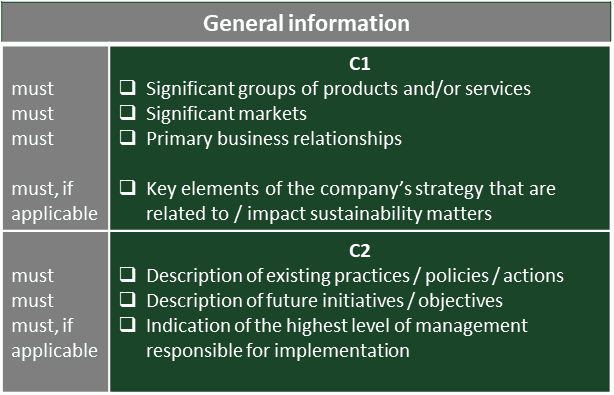

C1 Strategy: Business Model and Sustainability-related Initiatives

This requirement focuses on the link between the company’s business model and its sustainability efforts. Data points include key product and service categories, core markets, and primary business relationships.

It also describes elements of the strategy directly related to sustainability. The objective is to demonstrate how ESG is integrated into the core business rather than operating as a parallel initiative.

C2 - Practices, Policies, and Future Initiatives

This section elaborates on existing practices, policies, actions, and planned initiatives and targets. It also includes information about which management level holds overall responsibility.

The focus is on governance and implementation, providing insight into how sustainability is translated from ambition into action.

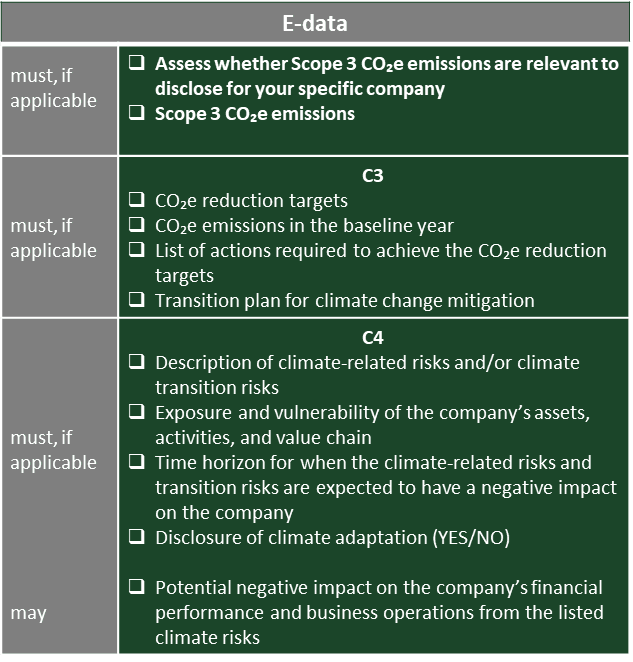

C3 - Targets for Greenhouse Gas Reduction and Climate Transition

The sub topic includes specific CO₂ reduction targets, baseline year definition, and actions to achieve targets, as well as overall climate transition plans. The focus is on direction and structure rather than full reporting complexity.

This sub topic also addresses Scope 3 emissions, which are voluntary under VSME and may be included where relevant or requested by stakeholders. Scope 3 covers indirect emissions across the value chain, such as purchased goods, transport, product use, and waste.

C4 - Climate Risks

This section identifies climate-related and transition risks affecting assets, operations, and the value chain. It includes exposure, vulnerability, and expected time horizon.

It may also include adaptation measures and assessments of financial and operational consequences.

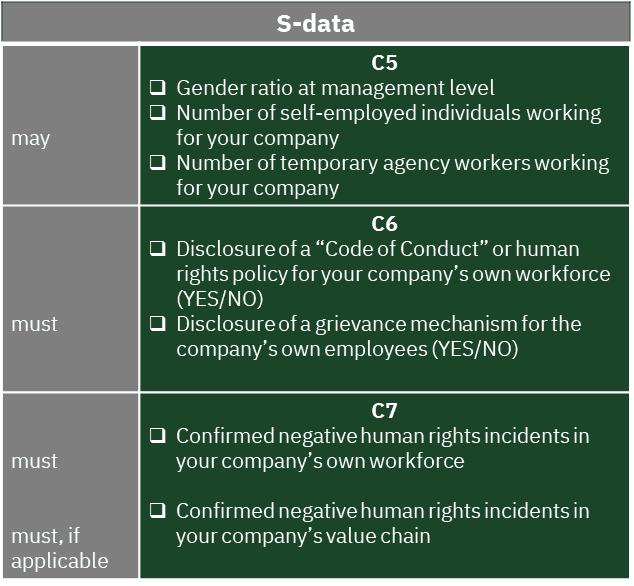

C5 - Supplementary Workforce Information

For companies with more than 50 employees, this requirement allows further elaboration on workforce-related disclosures, including gender distribution at management level and use of contractors.

C6 Own Workforce: Human Rights Policies and Processes

This section covers the company’s approach to human rights for its workforce, including whether a Code of Conduct or human rights policy exists and whether grievance mechanisms are available.

C7 - Severe Human Rights Incidents

This requirement covers confirmed severe human rights incidents in the undertaking’s own workforce and value chain.

The undertaking must disclose whether it has identified substantiated cases of child labour, forced labour, human trafficking, discrimination, or other serious violations, and whether it is aware of similar incidents in its value chain. If relevant, it may describe actions taken to address and prevent such incidents.

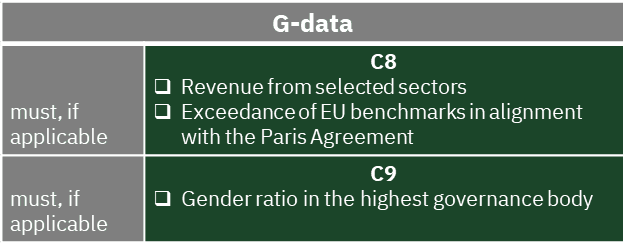

C8 - Revenue from Selected Sectors and Exclusion from EU Benchmarks

This section addresses whether the company derives revenue from specific sectors relevant from a sustainability perspective. It may include alignment with EU benchmarks and the Paris Agreement.

It also identifies whether the company operates in controversial weapons, tobacco, fossil fuels, or chemical production.

C9 - Gender Distribution in the Highest Governance Body

The module concludes with disclosure of gender distribution in the highest governance body, providing insight into leadership diversity.

VSME as a Strategic Management Tool

When applied with the right guidance, VSME becomes a central framework for ESG management. It helps create clarity, prioritise resources, and ensure that sustainability initiatives support overall corporate strategy rather than standing alone.

Get Started with VSME Together with Quantified Impacts

At Quantified Impacts, we specialize in ESG advisory and support companies in implementing VSME reporting.

We offer:

• A structured VSME report with a simple setup to help companies get started and build internal capabilities

• An ESG-data collection template directly aligned with VSME disclosure requirements

• An ESG-project that is suited for each customers individual starting point and ambition level

• A flexible workflow tailored to each customer’s needs — where some require us to take full responsibility for preparing and delivering the ESG report, while others need advisory support alongside an external ESG Manager.

• Support in developing an ESG strategy integrated into overall business strategy

• Training on how VSME can be used for branding, commercial value creation, and stakeholder requirement management

At Quantified Impacts, we do not see VSME as merely a report, but as a value-creating tool across the business without becoming a reporting burden.